Duty Drawback

- What is Duty Drawback?

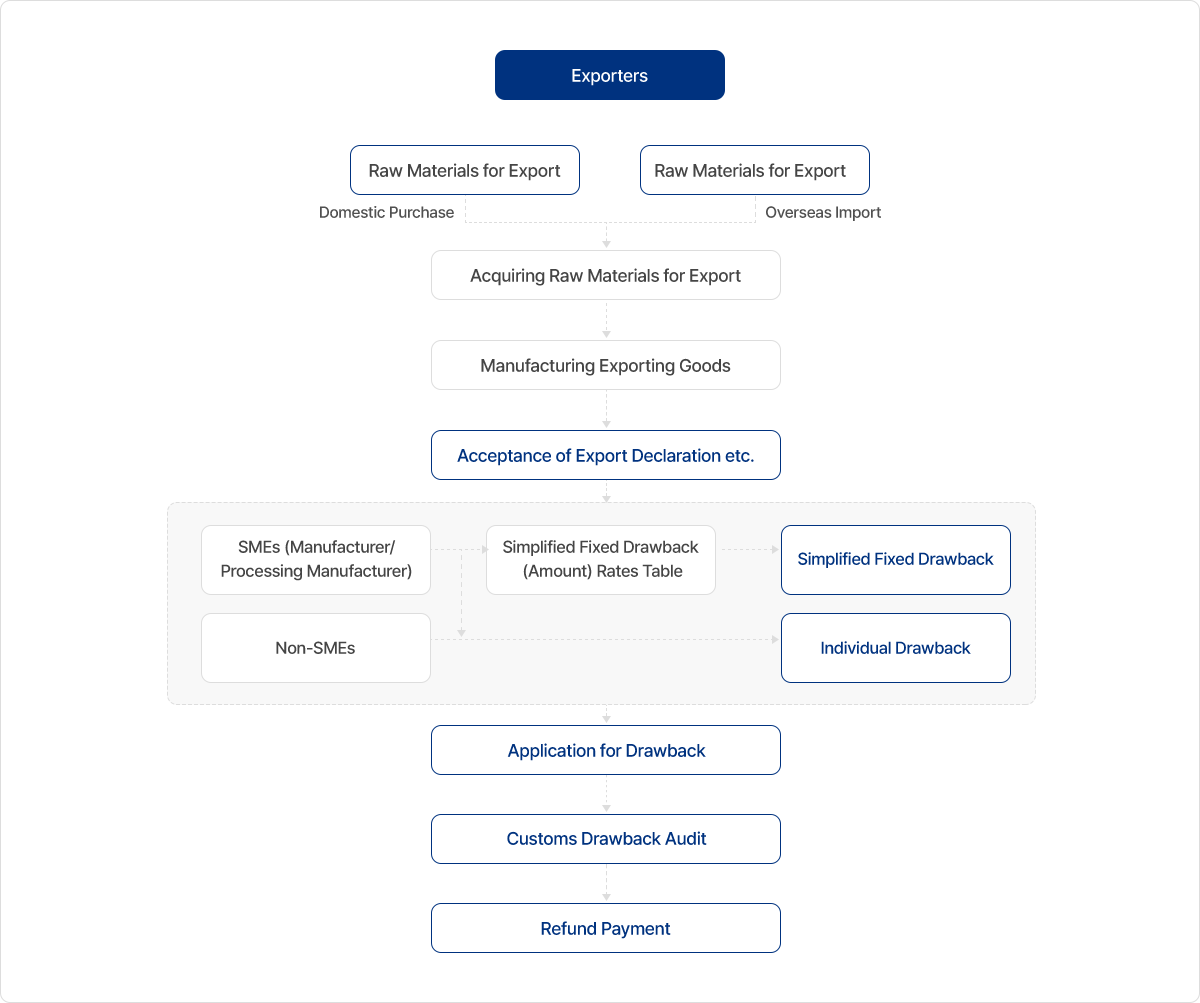

- It's the system to refund duties to the exporter or the manufacturer of exporting goods in accordance with 'Act on Special Cases Concerning the Refund of Customs Duties Levied on Raw Materials for Export' such as where the imported with tariff paid is exported after domestically manufactured

Duty Drawbacks

Individual Drawback

| Subject of Application | Applicable Items | Document to be Submitted |

|---|---|---|

| All Exporters | All Exporting Items | Affidavits for Export Certificate of Tax Amount Paid Calculation Bill of Yield Ratio |

| Refunding the yielded tax amount paid at the time of import of the raw materials used for the manufacture of exporting goods |

||

Simplified Fixed Drawback

| Subject of Application | Applicable Items | Document to be Submitted |

|---|---|---|

| Annual Refund for SMEs (Less than KRW 0.8 billion) |

Exporting items in Simplified Fixed Drawback (Amount) Rates Table |

Affidavits for Export |

| Refunding some amount per every KRW 10,000 of export amount in case of the export of the goods subject to simplified fixed drawback |

||

Individual Drawback Process

-

1Importing Raw

1Importing Raw

Materials- The amount of tax paid for the imported raw materials should be available.

- If the purchase was domestically made, the amount of paid tax should be proved with Certificate of Tax Payment on Raw Materials, Certificate of Split (or Partial) Tax-Payment on Import, or Certificate of Average Tax Amount etc.

-

2Manufacturing

2Manufacturing

Exporting Goods- Imported raw materials should be combined with the goods to be exported physically or chemically.

- The raw materials subject to drawback include consumed items to be used for exporting goods manufacturing process and packaging items of the exporting goods.

-

3Yield-Ratio

3Yield-Ratio

Calculation- Yield-Ratio for manufacturing exporting goods should be calculated by randomly selecting one of the six methods set forth in 'Notice of Yield-Ratio Calculation and Administration/Audit'.

-

4Application

4Application

for Drawback- The application should be made within 5 years from the day of supply for export etc.

-

5Paying Refund

5Paying Refund- The refund in application is paid to the claimant’s bank account after checking the filled-in information and the preparation of document to be submitted.

-

6urveillance

6urveillance

Audit- The refund should be audited for its accuracy of amount after it’s paid except where the claimant had been penalized for improper refund or there’s a risk of overpayment.

Overview of Drawback

Service Scope

| Individual Drawback Application | Simplified Fixed Drawback Application |

| Declaration (Amendment) of Yield Ratio Calculation | Refund Payment Application |

| Additional Drawback Application | Application for Issuance of Certificate of Average Tax Amount |

| Application for Issuance of Certificate of Tax Payment on Raw Materials | Application for Issuance of Certificate of Split |